Understanding Disability Insurance: Your Safety Net During Hard Times

Understanding disability insurance is crucial for safeguarding your financial future in the face of unexpected challenges. This type of insurance serves as a safety net during hard times, providing a source of income if you become unable to work due to illness or injury. Unlike health insurance, which covers medical expenses, disability insurance focuses on replacing a portion of your lost income, allowing you to maintain your standard of living when life takes an unexpected turn.

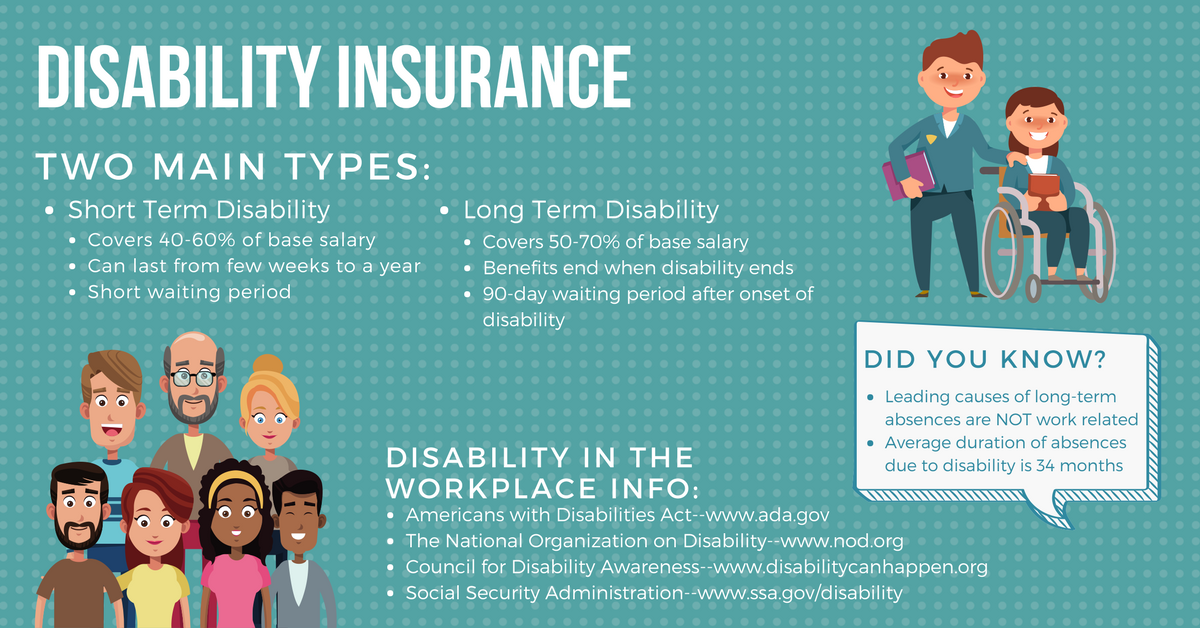

There are two primary types of disability insurance: short-term and long-term. Short-term disability insurance typically covers a portion of your income for a few months, while long-term disability insurance can provide benefits for several years or until retirement age. It’s essential to carefully evaluate your options and consider factors such as waiting periods, benefit amounts, and duration of coverage. Investing in disability insurance can be one of the best decisions you make, ensuring that you are financially prepared to weather any storm that comes your way.

Top 5 Ways Disability Insurance Can Protect Your Income

Disability insurance is a crucial financial safety net that ensures your income remains protected in the event of illness or injury that prevents you from working. By providing a replacement income, this type of insurance plays an essential role in maintaining your lifestyle and meeting financial obligations. Here are the top 5 ways disability insurance can protect your income:

- Income Replacement: Disability insurance typically covers a portion of your salary, allowing you to pay bills and support your family without the added stress of financial strain.

- Peace of Mind: Knowing that you have a plan in place to cover lost income can alleviate anxiety during challenging times, enabling you to focus on recovery instead of financial worries.

- Long-Term Protection: Many policies offer coverage that lasts for years or even until retirement age, providing ongoing support if a disability affects your ability to work long term.

- Supplemental Benefits: Some policies may include additional benefits like rehabilitation services or job placement assistance, helping you transition back to work successfully.

- Flexibility: Disability insurance policies can often be customized to fit your specific needs and financial situation, ensuring you get the coverage best suited for you.

Is Disability Insurance Worth It? Debunking Common Myths

When considering if disability insurance is worth it, many individuals are often influenced by common myths that downplay its importance. One prevalent misconception is that disability insurance is only necessary for those with physically demanding jobs. In reality, illness and injury can affect anyone, regardless of occupation. In fact, over 25% of today's workers will experience a disability for 90 days or more at some point in their careers, making a strong case for everyone to consider this financial safety net.

Another myth suggests that disability insurance is unnecessary because government programs provide sufficient coverage. However, these programs typically offer minimal benefits that may not meet one’s financial obligations during a period of disability. For example, the average Social Security Disability Insurance payment falls short of covering basic expenses, thus putting individuals at risk of financial instability. Therefore, investing in quality disability insurance can serve as a crucial tool in safeguarding your financial future.